The hardest part of any payoff plan is usually not the math—it is month four, when nothing feels different and the temptation to quit starts building. A debt snowball spreadsheet is built for exactly that problem. In this five-debt scenario, $24,650 of debt with $718 of required minimums and a repeatable $300 extra payment reaches zero in July 2028 under both snowball and avalanche. But snowball clears one balance in May 2026, a second in August 2026, and leaves only two open debts by March 2027. I verified the numbers by running the same stack through our debt payoff calculator.

What The Snowball Spreadsheet Should Tell You Right Away

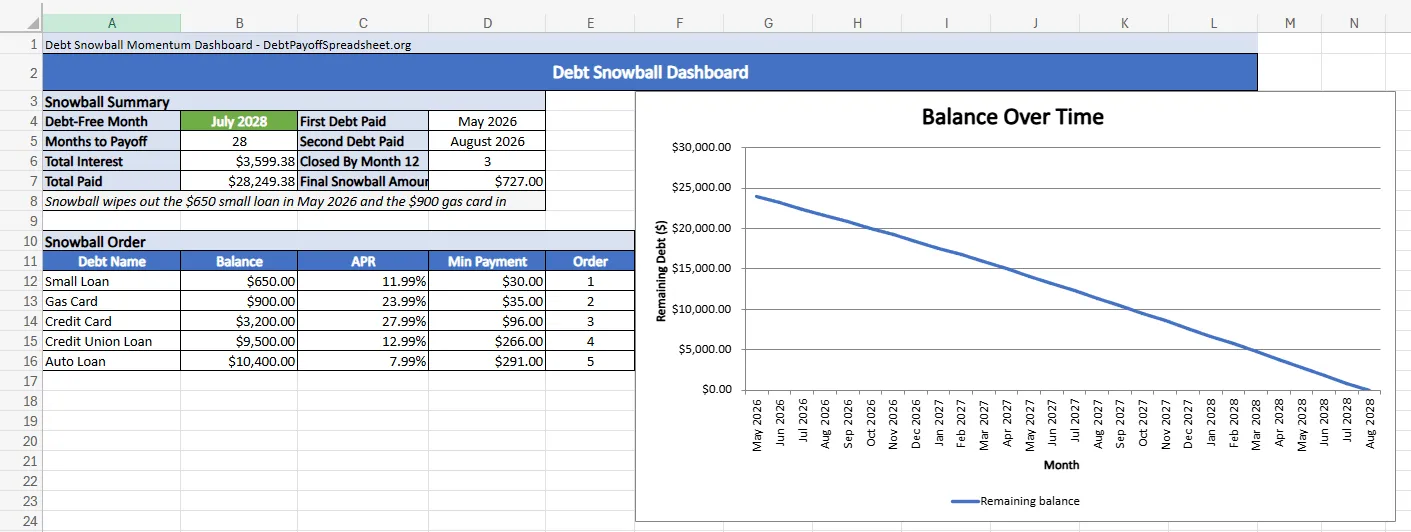

A useful snowball spreadsheet does more than sort balances from smallest to largest. It needs to show the monthly outlay, the debt-free month, the cost of interest, and the next payoff date that will make the plan feel simpler. In this scenario, the file starts with a $650 Small Loan, a $900 Gas Card, a $3,200 Credit Card, a $9,500 Credit Union Loan, and a $10,400 Auto Loan. The planned monthly outlay is $1,018, which is the $718 minimum-payment base plus the extra $300 you can repeat every month.

APR still matters even when you choose snowball. Most card issuers calculate interest using an average daily balance method, which means every day a high-APR card carries a balance costs real money (CFPB). Sending the extra payment to the smallest balance instead of the most expensive one has a price, and the spreadsheet needs to show that price clearly.

The dashboard on this page shows the exact shape of the plan: July 2028 in 28 months, $3,599.38 of interest, $28,249.38 paid overall, and a final snowball amount of $727 once enough minimum payments have rolled forward.

Why The Quick-Win Version Can Make Sense Here

In this exact debt stack, avalanche does not beat snowball on finish date. Both methods end in July 2028, and avalanche only saves $100.41 of interest. Snowball removes the Small Loan in May 2026 and the Gas Card in August 2026, while avalanche does not eliminate its first full balance until January 2027 because the $3,200 card absorbs the extra payment for most of the first year.

Peer-reviewed research published through Duke Scholars found that consumers often prefer eliminating smaller balances first, a pattern the authors call debt account aversion (Duke Scholars). That does not prove snowball is always the right call. But it helps explain why a reader looking for a debt snowball spreadsheet is usually not looking for the same thing as a reader who wants the strict highest-APR answer. Here, the quicker account-count drop costs $100.41, not extra years in debt.

Same Debts, Different Feel In Year One

Five debts, April 2026 start, $300 extra payment

| Metric | Snowball | Avalanche |

|---|---|---|

| First debt paid | May 2026 | January 2027 |

| Open accounts after 12 months | 2 | 3 |

| Debt-free month | July 2028 | July 2028 |

| Total interest | $3,599.38 | $3,498.97 |

| Total paid | $28,249.38 | $28,148.97 |

If you know you would rather aim extra money at the most expensive balance first, use the debt avalanche spreadsheet. If you are still deciding which method fits your temperament and cash flow, the broader debt payoff strategies guide is the better decision page.

Track The Snowball Amount, Not Just The Balances

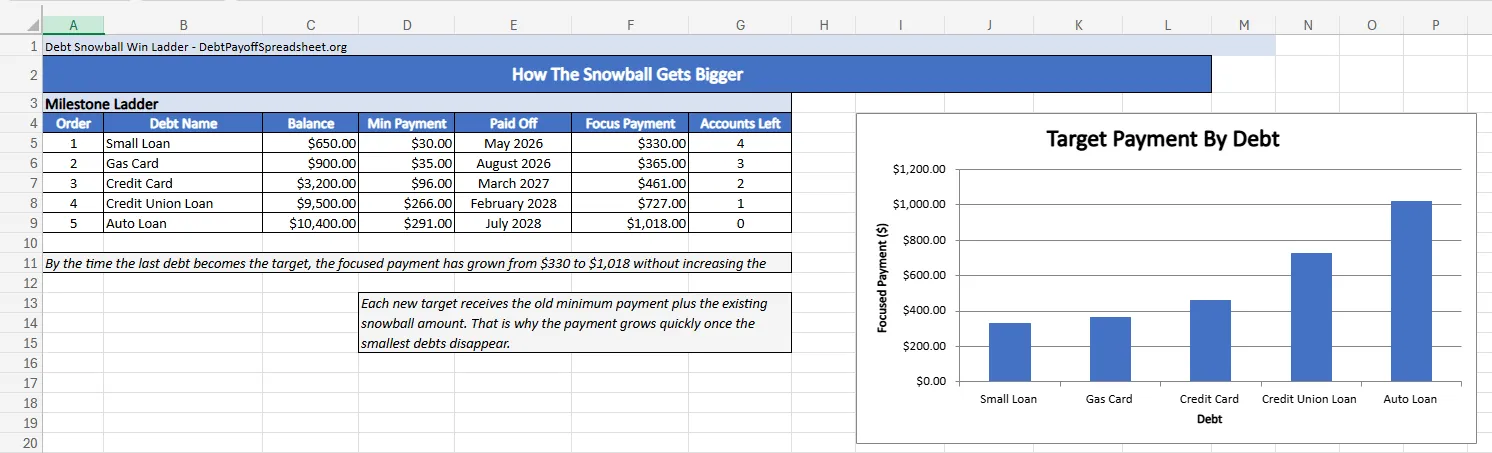

The mistake most homemade snowball sheets make is stopping at a sorted debt list. Each cleared balance frees up a minimum payment, and that minimum becomes part of the next target’s payment. In this scenario, the focused payment starts at $330 on the Small Loan, rises to $365 on the Gas Card, then to $461 on the Credit Card, then to $727 on the Credit Union Loan, and finally to the full $1,018 on the Auto Loan.

That ladder turns a vague payoff plan into concrete payment levels. By the time the Credit Card becomes the target, the worksheet is showing what the same monthly outlay looks like after two obligations have disappeared. Our how to create a debt payoff spreadsheet walkthrough covers this structure step by step if you prefer building from scratch.

Use The First-Year View To Catch Drift Early

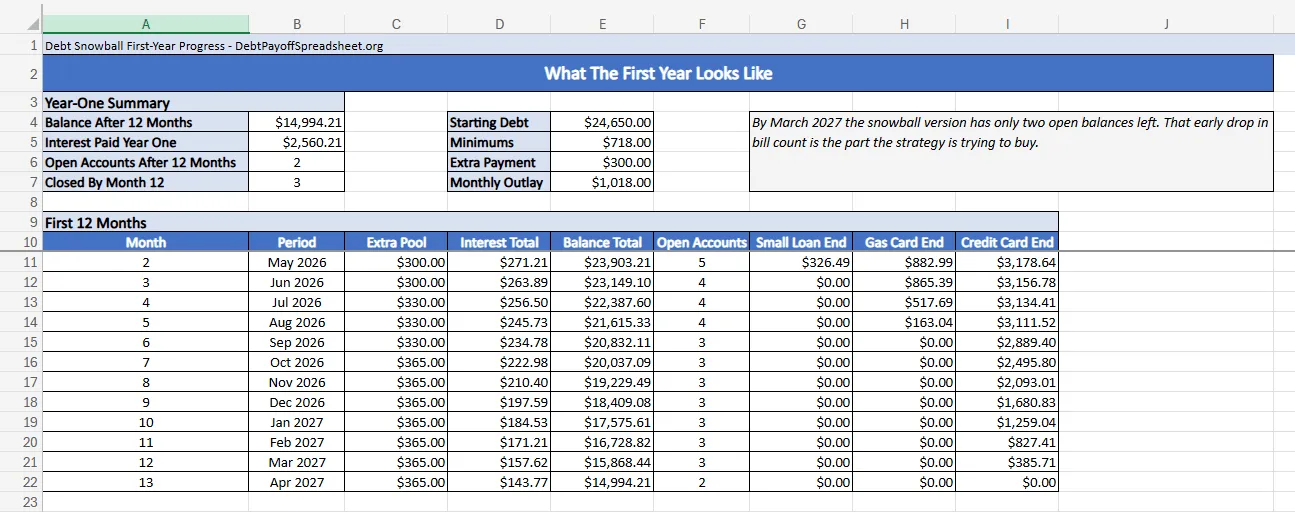

Snowball usually earns its keep in the first year. That is why the first-year table is more useful than a giant 28-month schedule when you are deciding whether the method feels sustainable. In this case, the ending balance falls to $14,994.21 by March 2027. Interest paid in that first 12-month stretch totals $2,560.21, and the number of open debts falls from five to two.

That account-count drop is where a spreadsheet beats memory. You can see the extra pool jump from $300 to $330 after the Small Loan disappears, then to $365 after the Gas Card is gone. If the balance trend is flatter than this example after a few statement cycles, you are either adding new debt, underfunding the extra payment, or working from stale balances and APRs. If two people need to review the file together every month, move the same logic into the shared Google Sheets tracker.

Edge Cases That Can Trip Up A Snowball Plan

No spreadsheet will match your next credit card statement to the penny. The CFPB explains that some credit cards use a daily periodic rate to calculate interest, so a monthly worksheet will not always match the statement’s interest line exactly (CFPB). The sheet is still useful as long as you update the live balance and APR after each statement closes.

Promotional debt is the bigger problem. The CFPB warns that minimum payments usually will not clear a deferred-interest purchase before the promotional period ends (CFPB). If your smallest balance is sitting on deferred-interest terms, blindly paying it first because it looks small can backfire. Rerun the numbers before the promo deadline and compare the snowball order against a rate-first alternative.

A debt snowball spreadsheet makes sense when early wins are what keep you going. In this scenario the price is only $100.41, and the finish month stays the same. If your own numbers show a wider gap, that is fine—the spreadsheet still did its job by surfacing the tradeoff before you locked yourself in.

Debt Snowball Spreadsheet FAQ

Is there a free debt snowball spreadsheet Excel download?

Yes. The homepage spreadsheet can be downloaded and used in Excel, and the files on this page are fixed snowball examples. Use the homepage file when you want a general template, and use these examples when you want to inspect a completed snowball setup first.

Can I use a debt snowball calculator in Excel?

Yes. Excel can handle the same snowball math if the workbook tracks each balance, APR, minimum payment, and one repeatable extra-payment amount. The real risk is using a file that does not roll freed minimum payments forward after a debt hits zero.

What is the debt snowball method?

The debt snowball method sends extra money to the smallest balance first while you keep making minimum payments on everything else. Each time a balance reaches zero, that minimum payment joins the next target and makes the focused payment larger.

Is a free debt snowball calculator enough, or do I need a spreadsheet?

A calculator is enough when you only need the payoff month and total interest. A spreadsheet is better when you want the month-by-month path, the closed-account count, and an easier way to review the plan after each statement cycle.