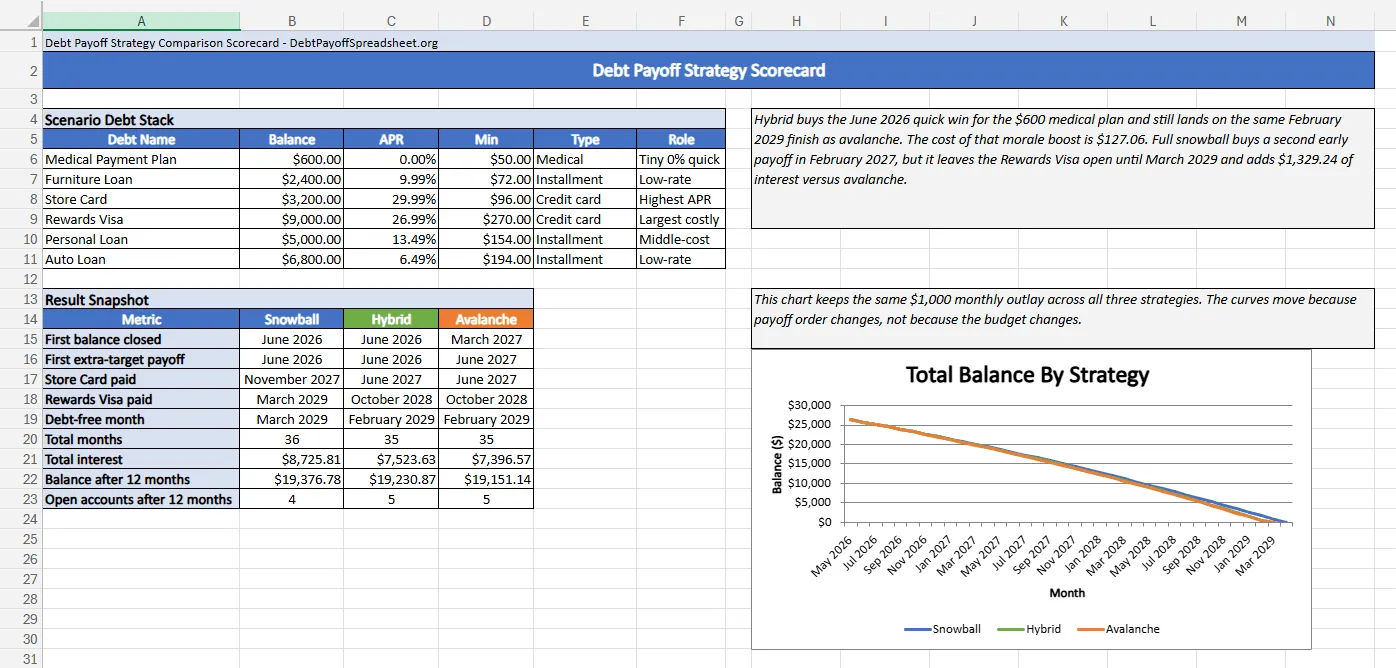

The real question behind every payoff method debate is not “which is mathematically best?”—it is “which one will I actually finish?” I ran this six-debt stack through our homepage debt payoff calculator starting in April 2026, and the three answers came back tighter than most people expect: snowball reaches zero in March 2029 with $8,725.81 of interest, avalanche reaches February 2029 with $7,396.57, and a one-win hybrid lands on that same February 2029 finish for $7,523.63. The right strategy depends on what you are buying with the extra cost.

The numbers matter because payoff order only works after the budget makes room for an extra payment. Your debt-to-income ratio—your monthly debt payments divided by your gross monthly income—is a quick way to tell whether that extra payment is realistic (CFPB). In this sample household, the extra payment is $164 on top of $836 of required minimums, which creates a steady $1,000 monthly outlay. That fixed outlay is what lets the strategy comparison stay clean.

Same Debt, Three Honest Answers

The debt stack is deliberately mixed because real payoff choices usually are. There is a $600 medical payment plan at 0.00%, a $2,400 furniture loan at 9.99%, a $3,200 store card at 29.99%, a $9,000 rewards card at 26.99%, a $5,000 personal loan at 13.49%, and a $6,800 auto loan at 6.49%. Month-one interest is $395.37, and $282.40 of that comes from the two credit cards alone.

That mix creates a useful tension. The smallest balance is cheap to carry and easy to erase. The biggest pain point is not the smallest balance at all. It is the $9,000 rewards card and the 29.99% store card that keep charging while you are busy elsewhere. That is why a broad article on debt payoff strategies should not stop at “snowball is motivating, avalanche saves money.” The real question is how much motivation you are buying, and whether the price is low, moderate, or reckless in your own debt mix.

Three Strategies, One Budget

Six debts, April 2026 start, $164 extra payment, $1,000 monthly outlay

| Metric | Snowball | Hybrid | Avalanche |

|---|---|---|---|

| First balance closed | June 2026 | June 2026 | March 2027 |

| Store Card paid | November 2027 | June 2027 | June 2027 |

| Rewards Visa paid | March 2029 | October 2028 | October 2028 |

| Debt-free month | March 2029 | February 2029 | February 2029 |

| Total interest | $8,725.81 | $7,523.63 | $7,396.57 |

| Open accounts after 12 months | 4 | 5 | 5 |

Snowball buys two early psychological wins. It wipes out the medical plan in June 2026 and the furniture loan in February 2027. Avalanche buys the cheapest total path, but it does not close any balance until March 2027, and that first closure is the medical plan hitting zero on minimum payments rather than a true rate-first victory. The one-win hybrid sits in the middle: clear the $600 medical plan first, then turn rate-first. In this exact case, that compromise costs only $127.06 compared with avalanche and does not change the finish month.

Avalanche Is The Clean Default When The Costly Card Is Also Large

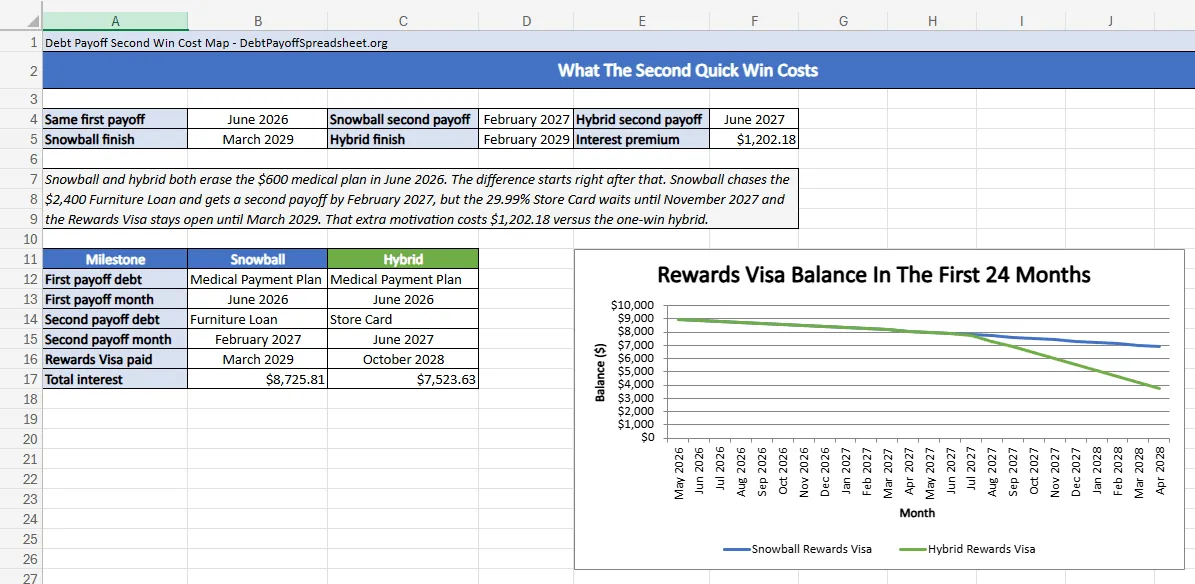

Avalanche earns its reputation when the expensive balance is not only high-rate but also heavy enough to stay around for a long time. That is exactly what happens here. The store card and rewards card start out small enough to feel manageable on paper, but together they drive most of the interest drag. By October 2028, avalanche has the rewards card gone. Under snowball, that card lingers until March 2029.

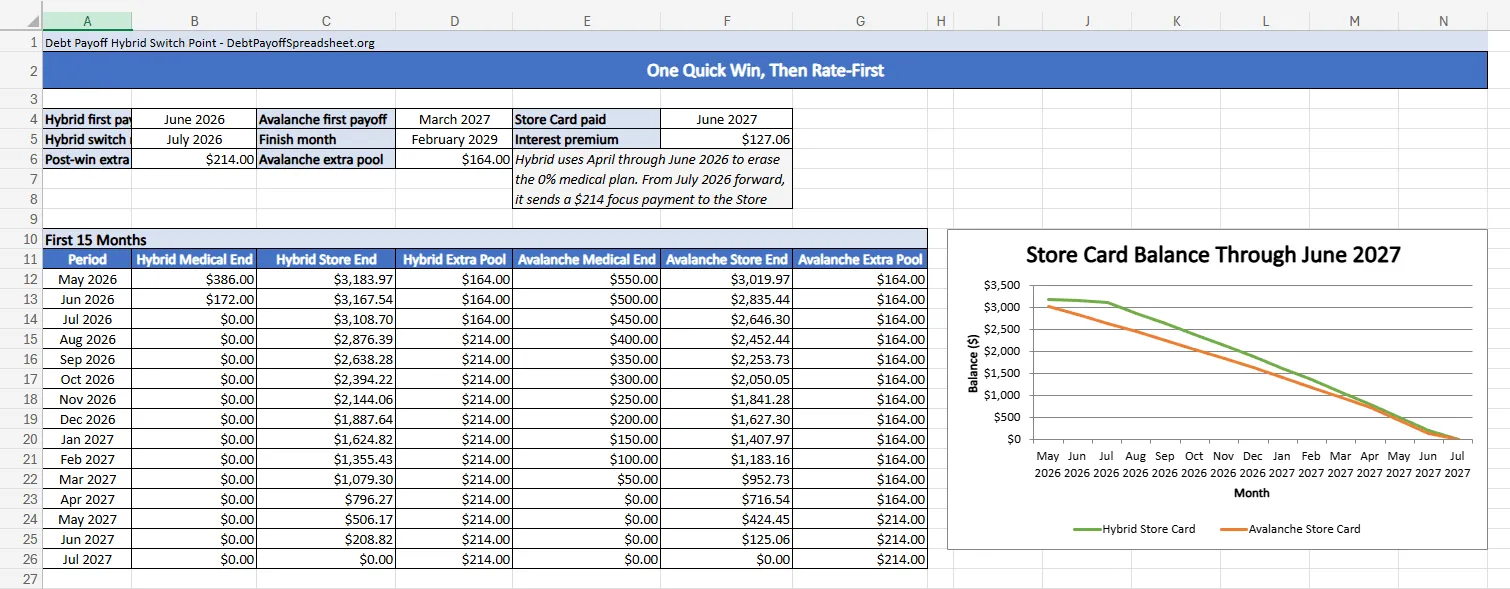

That is why a first closed account can be misleading. Under avalanche, the first balance to disappear is the 0.00% medical plan in March 2027. That does not mean avalanche secretly behaves like snowball. It means a tiny low-cost balance can amortize itself away while the extra payment keeps attacking the Store Card. The first real rate-first payoff is still the Store Card in June 2027.

Readers who know they care most about interest cost should move to the debt avalanche spreadsheet after reading this page. If most of your debt is revolving card debt, also check the credit card debt payoff guide before locking in a long order, because a large high-APR card is often the balance that quietly decides whether avalanche meaningfully outperforms everything else.

A One-Win Hybrid Makes Sense When The Smallest Debt Is Cheap

The best surprise in this scenario is how little the first quick win costs if you stop after one. Hybrid pays off the $600 medical plan in June 2026, then shifts to rate-first order in July 2026 with a $214 focused payment instead of avalanche’s $164. That larger focused payment is enough to keep the Store Card on the same June 2027 payoff date avalanche gets, even though avalanche started hitting it with extra dollars from month one.

That pattern matters more than the label. Plenty of people do not need repeated wins. They need one early sign that the system works. If the smallest balance is also low or zero interest, taking it out first can be a rational buy instead of an emotional mistake. In this case, the price of that confidence is $127.06.

This is also the section where experience matters. A lot of payoff advice treats every early win as equally valuable. They are not. A one-win hybrid works here because the medical plan is tiny and free to carry. If the smallest debt were the 29.99% store card or a larger card balance with real interest pressure, the same compromise would be much harder to defend.

Snowball Only Earns Its Place If The Second Quick Win Matters More Than $1,202.18

Snowball has a serious behavioral case, and pretending otherwise is lazy. Research published through Duke Scholars found that consumers often favor smaller balances first even when interest-rate logic points elsewhere (Duke Scholars). That helps explain why snowball feels easier to trust in month two, before the lower-interest math has had time to feel real.

The same research does not mean every quick win is worth the same price. In this scenario, snowball and hybrid already share the first payoff in June 2026. The extra cost appears because snowball keeps going after the $2,400 furniture loan instead of pivoting toward the Store Card. That choice buys a second payoff in February 2027, but it leaves the Store Card open until November 2027 and the Rewards Visa open until March 2029.

If that is the kind of momentum you know you need, own the tradeoff instead of hiding from it. Snowball adds $1,202.18 of interest versus the one-win hybrid and $1,329.24 versus avalanche. It also finishes one month later. For some readers, that is still worth paying. For others, it is the point where motivation becomes too expensive.

If you want to work from a motivation-first template after making that call, try the debt snowball spreadsheet. If your priority is staying aggressive without paying for every future quick win, the hybrid logic on this page is closer to the real compromise.

The Limits Of Picking A Strategy

Payoff order matters, but it does not solve everything. If your budget cannot keep the extra payment alive, all three methods weaken at the same time. If new card spending continues, the best strategy on paper turns into a moving target. Variable APRs can also reshuffle the ranking while you are in the middle of the plan—rates move with the market, so a payoff order should be revisited whenever card terms shift (CFPB).

That is the practical limit of any strategy article. It can tell you where the extra dollar should go. It cannot create the extra dollar, freeze a variable card rate, or protect the plan from new balances. For the budget side, see the how to pay off debt fast guide. For revolving-debt edge cases, the credit card debt payoff guide goes deeper.

For this exact six-debt stack, the cleanest decision rule is simple. Choose avalanche if you can tolerate a long wait before the plan feels easier. Choose the one-win hybrid if one fast proof point will keep you engaged and $127.06 feels like a fair price. Choose full snowball only if the second fast payoff is important enough to justify $1,202.18 more than the hybrid and $1,329.24 more than avalanche.

Debt Payoff Strategies FAQ

How do I pay off debt quickly?

Paying off debt quickly usually comes down to two things: keeping a repeatable extra payment in the budget and aiming that extra money in a deliberate order. In the scenario on this page, the fastest finish comes from avalanche or a one-win hybrid, not from full snowball. If the budget cannot support the extra payment consistently, changing order alone will not solve the problem.

How to pay off debt fast?

Start by listing each balance, APR, and minimum payment, then compare at least two payoff orders before you commit. Fast payoff is not only about the biggest monthly push. It is also about not wasting that push on a balance that costs little to carry while an expensive card keeps compounding.

How to pay off debt?

Pick one method, keep minimum payments current on every debt, and send all extra money to one target at a time. The better method is the one you can keep following after the first hard month, not the one that only looks best in theory. That is why this article compares motivation and cost on the same numbers instead of treating strategy as a personality quiz.

What is the debt snowball method?

The debt snowball method sends extra money to the smallest balance first while you keep making minimum payments on everything else. Every time a balance reaches zero, that minimum payment rolls into the next target and makes the focused payment larger. It can work well when the early account closures are what keep you engaged, but it often costs more interest than avalanche.

Related Guides and Resources

- Debt Payoff Calculator: Compare Snowball vs Avalanche Before You Commit

- How to Create a Debt Payoff Spreadsheet From Scratch

- Budget and Debt Payoff Spreadsheet: One File for Spending, True Expenses, and Debt Targets

- Debt Payoff Spreadsheet Printable: Free Print-Ready Tracker With Monthly Check-In Sheets