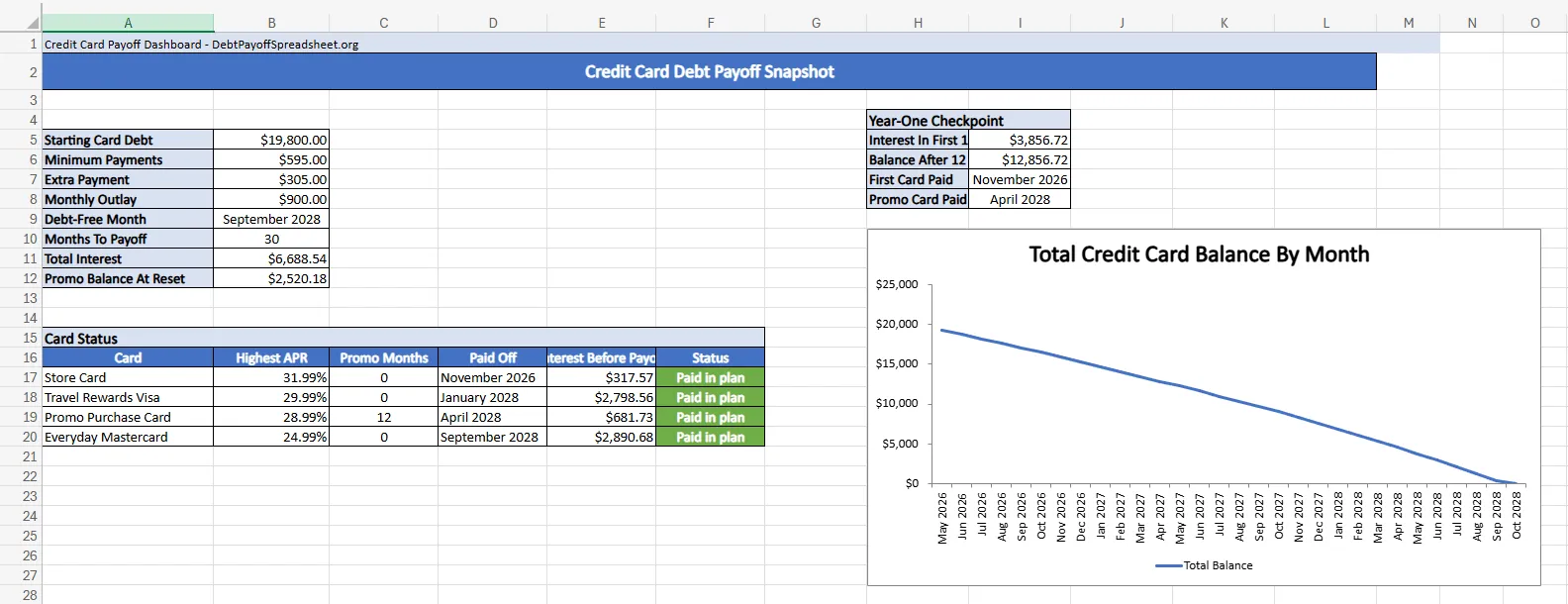

Credit card debt payoff gets tricky faster than a mixed debt plan because the rules can change while you are still making the first few payments. Four cards, $19,800 total, $595 in minimums, and a repeatable $305 extra payment keeping the monthly outlay at $900. I ran those balances through our homepage debt payoff calculator and the order came back clean: Store Card first, then Travel Rewards Visa, then Promo Purchase Card after its reset, then Everyday Mastercard. September 2028 is the debt-free month—but the promo deadline and the balance-transfer question still need answers before you do anything next month.

What A Card-Only Payoff Plan Needs To Show

The first surprise in this scenario is that the best opening move does not feel abstract at all. The Store Card is both the smallest balance and the highest APR, so the plan gets its first full payoff in November 2026 without paying a motivation premium for it. From there, the Travel Rewards Visa stays in the hot seat until January 2028, the Promo Purchase Card drops in April 2028, and the Everyday Mastercard is the last card standing until September 2028. Total interest comes to $6,594.53.

Card debt deserves its own payoff guide because the monthly plan is not just balance plus APR plus discipline. Minimum payments, late fees, and penalty repricing all interact. The minimum is the amount you must pay each month; paying more reduces interest; and a missed or late minimum can trigger a higher APR or cancel an introductory rate early (CFPB). If one of your cards is already late, getting current comes before optimizing the order, because the cheapest plan on paper is useless once the issuer has repriced the account.

This exact debt mix also shows why generic snowball-versus-avalanche language can miss the point. Here, the first win arrives quickly even though the plan is still cost-conscious. If your own smallest card is not also your most expensive balance, the debt payoff strategies guide covers the decision rules in more depth.

Promo APR Deadlines Belong In The Plan From Day One

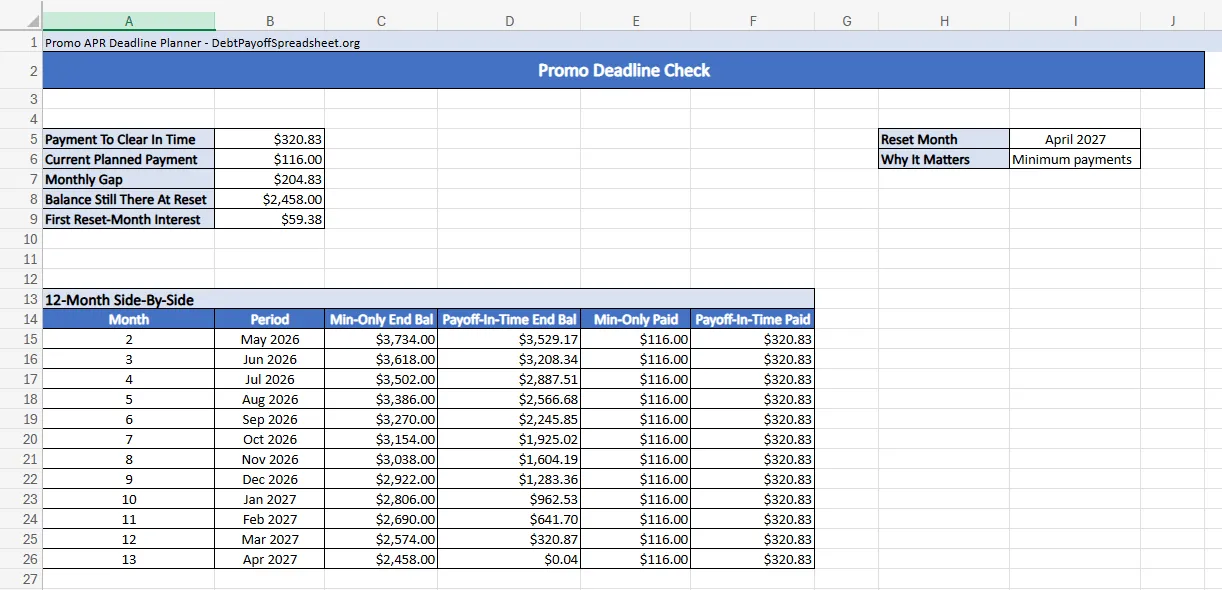

The Promo Purchase Card is the quiet risk in this stack. While the intro rate is still 0.00%, it makes sense to leave the extra payment on more expensive cards. That does not mean the promo balance is harmless. To clear $3,850 before the reset date, the card would need $320.83 per month. The current minimum is only $116, which leaves a $204.83 monthly gap. If nothing changes, the balance sitting there when April 2027 arrives is $2,458.00, and the first month after the reset adds $59.38 of interest by itself.

That is the practical rule for promo cards: they do not have to be first in line today, but they do need a calendar date inside the plan. The CFPB says an introductory rate must stay in effect for at least six months unless you are more than 60 days late, and the issuer has to disclose both how long the intro rate lasts and what rate comes next (CFPB). In other words, the deadline is knowable. If your tracker is not showing it, the tracker is the problem.

This is also where card-heavy payoff plans diverge from a simple rate-first workbook. The Travel Rewards Visa still deserves the extra payment while it is charging 29.99%, but the moment a new statement, fee, or promo reset changes the ranking, the plan needs a fresh run. If your balances are stable and you mainly need a rate-first tracking file, the debt avalanche spreadsheet covers that angle.

A Balance Transfer Only Counts If The Fee Gets Recovered Quickly

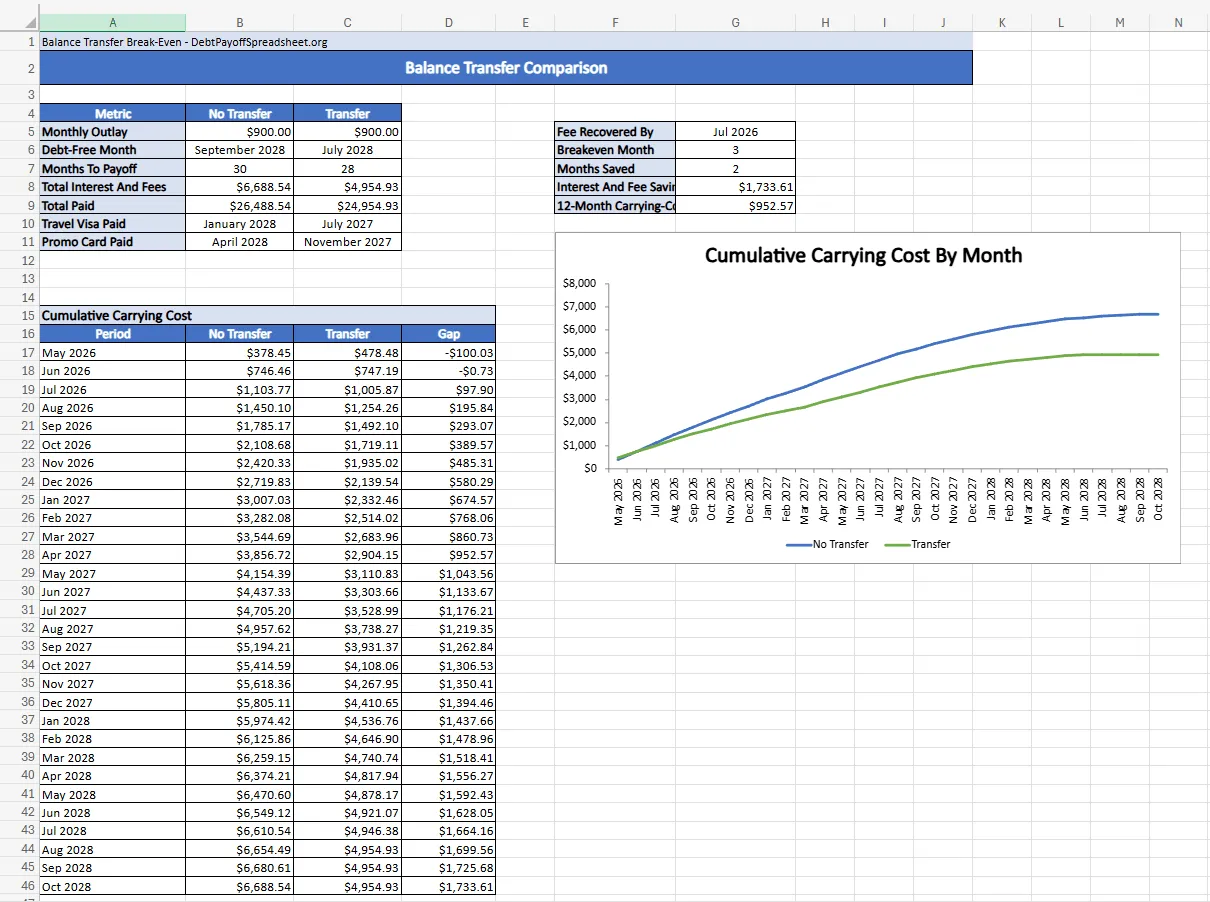

A transfer offer earns its place only when it changes the math after the fee, not before it. In this scenario, moving $4,000 from the Travel Rewards Visa to a new card with 15 months at 0.00% adds a $200 fee and raises required minimums from $595 to $601. To keep the household at the same $900 outlay, the extra-payment bucket drops from $305 to $299. Even with that restraint, the transfer version reaches zero in July 2028 instead of September 2028 and cuts interest-and-fee drag from $6,594.53 to $4,606.76. The gap is $1,987.77.

The timing matters almost as much as the final savings. In this model, the transfer fee is recovered by June 2026, the third payment month, and the transfer plan is ahead by $952.57 after the first year. That is the kind of breakeven you want. If a transfer offer does not pay back its fee quickly on a high-APR balance, it is usually solving the wrong problem.

Two card-specific cautions belong next to those savings. The CFPB notes that issuers can charge a balance transfer fee even on a 0% offer (CFPB). It also warns that if you carry a balance month to month, new purchases on that same card can start accruing interest immediately even while the transferred balance itself still has a low or zero promotional rate (CFPB). A transfer card only stays cheap if it stays quiet.

Card Payoff Plans Go Stale Faster Than Loan Plans

The useful takeaway here is not that every card stack needs a transfer or that every promo balance should leap to the front. It is that credit card debt payoff has more moving parts than a plan built mostly from fixed loans. Statement balances drift. Minimums shift. Promotional windows close. One careless swipe on the wrong card can undo a month of progress.

That is why the tracking habit matters as much as the original payoff order. For a desktop file you maintain alone, the Excel debt payoff spreadsheet is a cleaner fit. If a partner needs the same numbers and the same review date, try the Google Sheets debt payoff tracker. Either way, the real job is the same: refresh balances after each statement, check the next promo deadline, and make sure the extra payment is still landing on the card that costs the most to leave alone.

On this exact stack, the clean rule is simple. Keep the rate-first working order because it already gives you an early win on the Store Card. Treat the promo end date as a checkpoint you have to revisit, not as a footnote. Take the transfer only when the fee is recovered quickly and the card will not pick up new purchases while the promotional balance is still there.

Credit Card Debt Payoff FAQ

Is there a credit card payoff spreadsheet?

Yes. The main spreadsheet on our homepage is the better fit if you want one file for your own balances, APRs, minimum payments, and extra payment amount. The workbook downloads in this article are narrower on purpose: they show one card-heavy scenario so you can inspect a promo deadline and a balance transfer decision before building your own plan.

Do I need a debt payoff planner Excel file if all my debt is on credit cards?

Usually, yes, if you want an offline file you can update after each statement closes. Credit card debt changes faster than a loan-only plan because promo periods end, minimums shift, and transfer offers add fees and new terms. If you prefer a live browser-based file instead, the same structure works in Google Sheets as long as you keep the card details current.

Can I use a debt payoff calculator Excel workbook for credit cards?

Yes, but the cleaner workflow is usually to use both the calculator and a workbook. On this site, the calculator gives the fast answer on payoff month, total interest, and which card should get the extra payment today. Excel or Sheets makes more sense once you want the month-by-month path and a record of statement changes, which matters more for cards than for fixed loans.

What should an Excel debt payoff template include for credit cards?

At minimum, it should have one row per card with balance, current APR, reset APR, promo months left, and minimum payment. A stronger template also includes one extra-payment field, a payoff schedule, and a clear flag for the next promo deadline. If you are comparing a balance transfer, the fee and the new card's post-promo APR need their own fields too.