A printed tracker sounds old-fashioned until your phone is the same device that opens the shopping app. Separating the plan from the screen that creates temptation is the whole point. In this four-debt scenario, $14,800 total, $545 in minimums, and a $255 extra payment keeping the monthly outlay at $800. I ran the numbers through our homepage debt payoff calculator starting in April 2026: the plan reaches zero in August 2028 under avalanche with $2,917.35 of interest, or the same August 2028 under snowball with $3,191.89.

A printed debt payoff spreadsheet works when the tracking rhythm is simple and the debts are not shifting underneath you. Most card issuers calculate interest using an average daily balance, so the monthly figure on your printout will be close but not exact (CFPB). As long as the rates stay stable and you are updating balances monthly, paper can keep you honest. It assumes the debt order is already settled and turns that answer into three print-ready sheets instead of another tool that tries to do every job at once.

What The Printable Page Should Show At A Glance

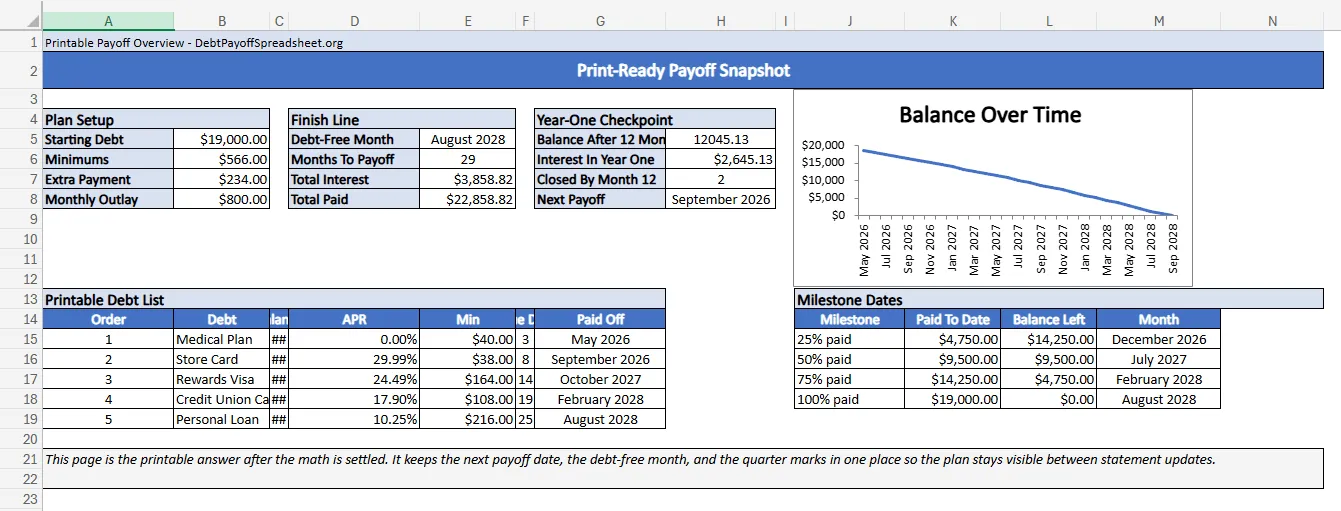

The first page should answer four questions without scrolling or mental math: what you owe, what you pay each month, which debt goes next, and when the plan ends. In this sample packet, the order is Medical Plan, Store Card, Rewards Visa, Credit Union Card, and Personal Loan. That means the Medical Plan is gone in May 2026, the Store Card drops off in September 2026, the Rewards Visa lasts until October 2027, the Credit Union Card ends in February 2028, and the Personal Loan is the final balance in August 2028. Total interest comes to $3,858.82.

That is enough information for a printed summary to stay useful on a fridge, desk, or binder cover. It does not need every formula on the page. It does need the debt-free month, the total monthly outlay, the next payoff date, and a few milestone dates you can glance at in ten seconds. If you have not actually chosen the debt order yet, stop here and use the debt payoff strategies guide first. Printing a plan before the plan is settled just gives you a prettier version of the confusion.

The Monthly Sheet Is The One You Actually Need

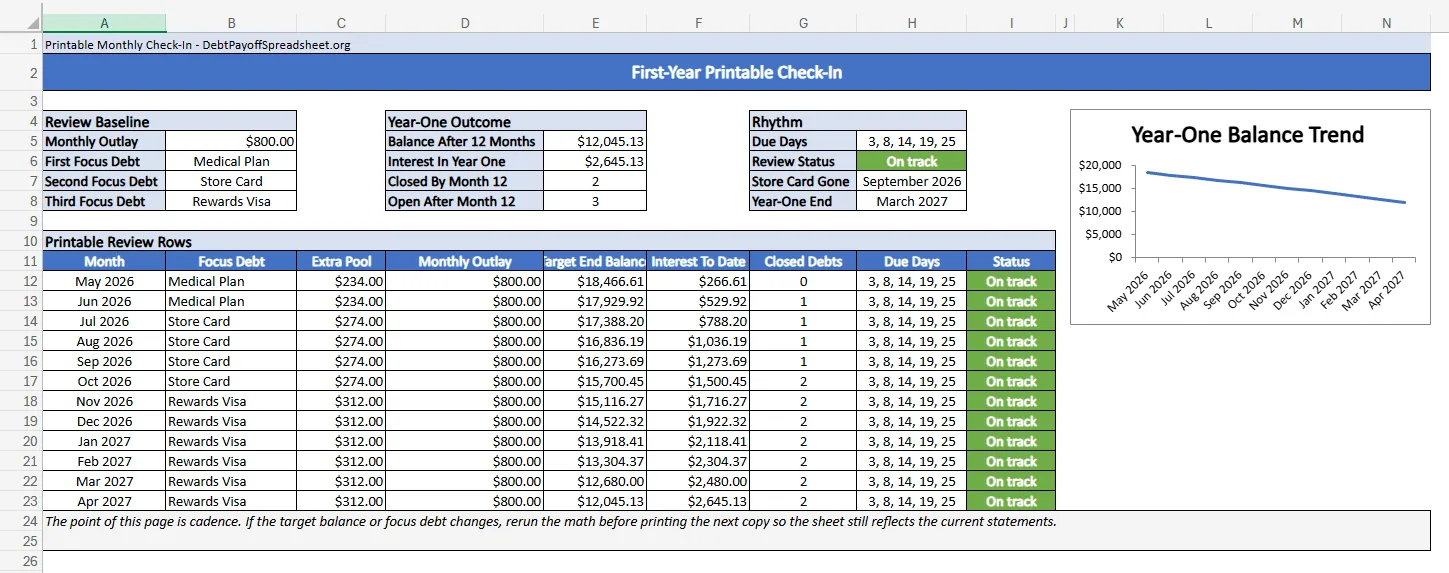

The overview gets attention, but the monthly sheet is the page that keeps the plan honest. In the first year of this scenario, the ending balance falls from $18,466.61 in April 2026 to $12,045.13 by March 2027. Interest paid to date reaches $2,645.13 by that twelfth check-in. The extra pool stays at $234 for the first two months, rises to $274 from June through September once the Medical Plan is gone, and then rises again to $312 from October 2026 forward after the Store Card disappears.

That is why a printable debt payoff worksheet should include due days and a review cadence, not just progress bars. The CFPB’s bill-calendar guidance recommends tracking what each bill is, what you owe, and when it is due so you know which bills are coming next (CFPB). The printed review sheet on this page does exactly that. It keeps the month label, current focus debt, extra pool, target ending balance, cumulative interest, and due-day pattern on one page, which is enough structure for a monthly review without turning the review into a spreadsheet session.

For readers who want the scorecard logic in a method-specific digital workbook, the debt snowball spreadsheet and debt avalanche spreadsheet track the same milestones with auto-updating formulas.

A Visible Progress Board Keeps The Plan In Sight

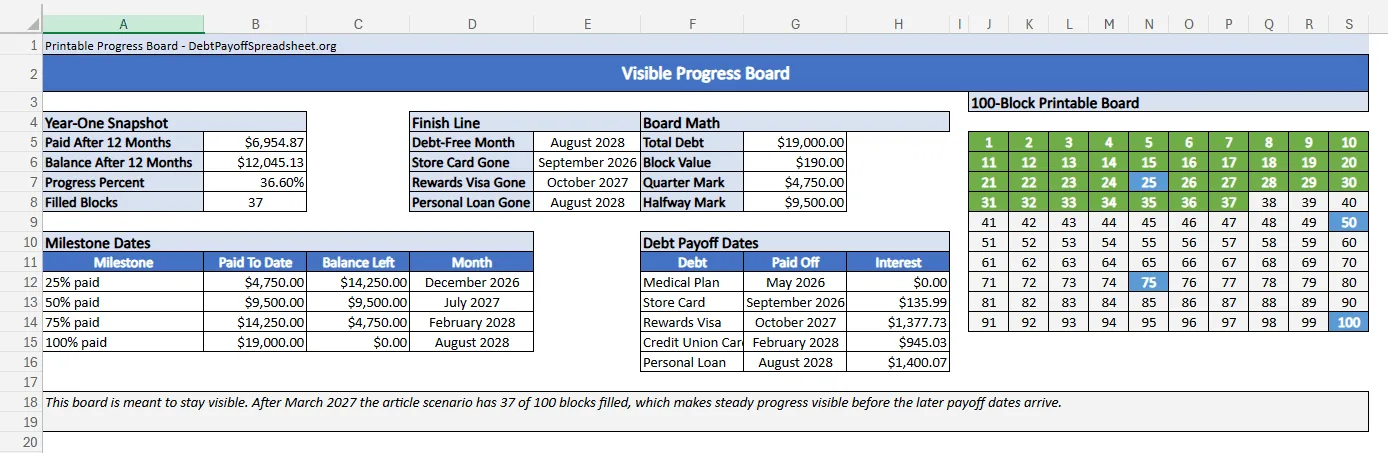

The third sheet exists for one reason: long payoff plans feel slow even when they are working. Here, the board turns the $19,000 starting balance into 100 blocks worth $190 each. By March 2027, the plan has paid down $6,954.87, which means 37 blocks are filled and 36.60% of the total balance is gone. The milestone dates stay clean too: 25% paid in December 2026, 50% in July 2027, 75% in February 2028, and the last block in August 2028.

That makes the board useful in a different way than the monthly check-in. The review sheet is for accuracy. The board is for visibility. It lets you see that the slow middle stretch is still moving even before the last large loan starts to collapse. For readers who need live recalculation, the Excel debt payoff spreadsheet handles the same plan in a formula-driven file. For two-person households, the Google Sheets version adds real-time sharing. But if what keeps you engaged is physically writing down the payment each month, start with the printable.

When Paper Reaches Its Limits

No printable tracker recalculates for you. When an APR changes or a promotional rate expires, you need to run the new numbers through a calculator or spreadsheet to see whether the order still holds. Deferred-interest offers are the worst case: minimum payments usually will not clear the balance before the promotional period ends, which means the interest can be charged retroactively (CFPB). That is normal. The answer is not to abandon the printable sheet. The answer is to update the balances and APRs after each statement closes so the next printout still reflects reality.

If your debt stack is mostly revolving card balances with variable APRs or looming promo expirations, the credit card debt payoff guide walks through those timing decisions. A printable plan is strongest for fixed-rate loans and stable card balances where the payoff arithmetic does not change every billing cycle.

Printable Debt Payoff Spreadsheet FAQ

Is there a free debt payoff worksheet I can print?

Yes. The spreadsheet on our homepage is the better general template if you want one file to customize from scratch, and the downloads on this page are print-ready examples built around one finished scenario. They are useful when you want to see what a printable debt payoff worksheet should look like before you build or adapt your own.

Can I print a debt payoff planner from Excel?

Yes. Excel works fine for a printable debt payoff planner as long as the sheet is laid out to fit on one page and the core numbers stay readable in landscape view. The files on this page are built that way, so you can print them directly or save them as PDFs after checking that the balances and payment amount still match your plan.

What should a printable debt payoff spreadsheet include?

It should show each debt's balance, APR, minimum payment, due day, the monthly outlay you can actually sustain, the next payoff date, and a few milestone dates so the plan does not feel endless. A printable tracker that skips any of those pieces usually turns into a motivational page without enough math behind it.

Should I use a printable tracker or a debt payoff calculator?

Use the calculator first when you still need to compare methods, pressure-test an extra payment, or confirm the debt-free month. Use the printable tracker after that, when the main job is keeping the plan visible between statement updates and monthly reviews.