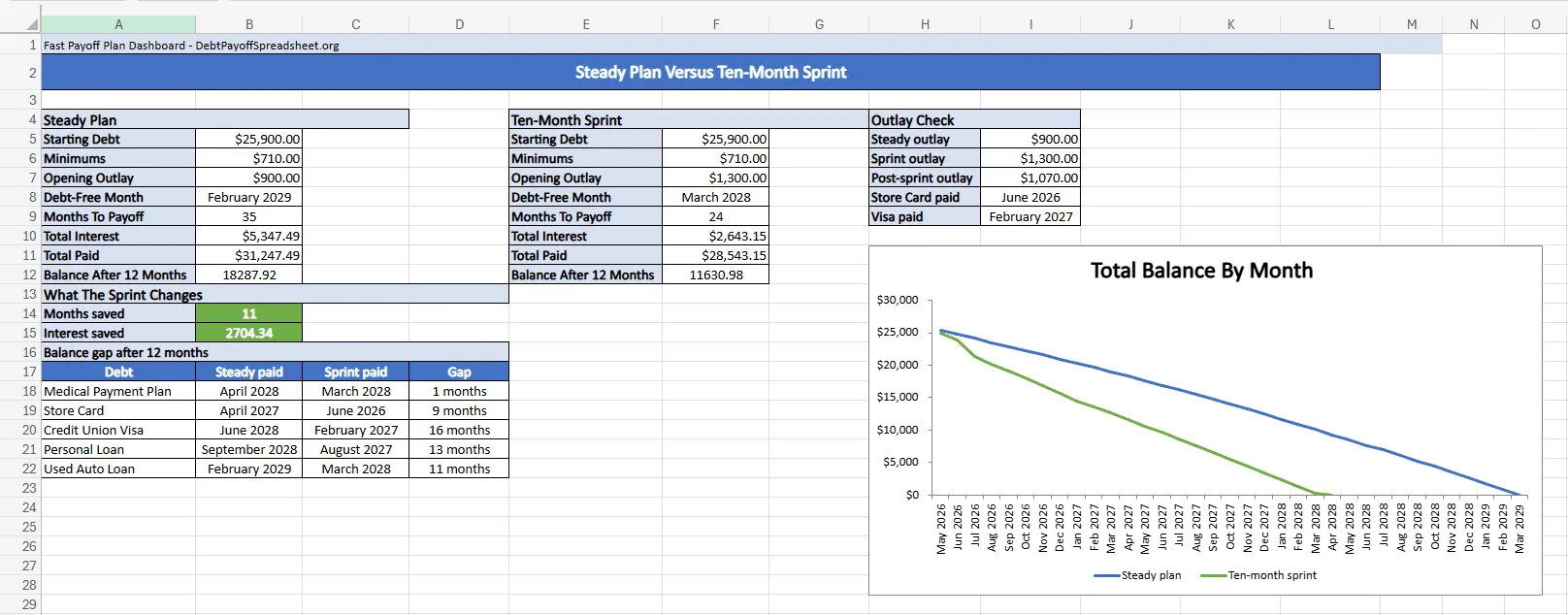

Once you know which balance gets the extra dollar, paying off debt fast stops being a strategy problem and becomes a cash-flow problem. In this five-debt stack, a steady $900 monthly outlay reaches zero in February 2029. Same balances, same rate-first order, but add a ten-month sprint, a $1,600 tax refund in July 2026, and the finish line moves to March 2028. I ran both versions through our homepage debt payoff calculator to verify: 11 months sooner and $2,674.34 less interest.

That gap shows what “fast” usually means in real life. While you carry a balance, you lose the grace period on new purchases—meaning interest starts accruing from the day the charge posts, not the statement due date (CFPB). The debt order matters, but order alone does not create speed. If you still need to choose between snowball, avalanche, or a hybrid, read the debt payoff strategies guide first. This page assumes the order is already set and asks a narrower question: how much faster can the same plan move if you front-load the cash?

Fast Payoff Starts With The Payment Stream

The debt stack here is mixed on purpose: a $1,100 medical payment plan at 0.00%, a $2,900 Store Card at 28.99%, a $6,400 Credit Union Visa at 24.99%, a $5,800 personal loan at 12.49%, and a $9,700 used auto loan at 6.24%. Minimum payments total $710. Under the steady plan, the household adds $190 and keeps the outlay at $900. Under the sprint plan, the debt order stays the same but the payment stream changes shape: $1,300 for the first ten months, then $1,070 after the temporary income ends.

That single shift changes the whole timeline. The steady plan keeps the Store Card alive until April 2027 and the Visa until June 2028. The sprint kills the Store Card in July 2026 and the Visa in February 2027. By the end of the first year, the steady plan still carries $18,287.92 of debt. The sprint is down to $11,529.80.

Same Debts, Different Speed

Five debts, April 2026 start, same debt order in both plans

| Metric | Steady plan | Ten-month sprint |

|---|---|---|

| Opening outlay | $900.00 | $1,300.00 |

| Post-sprint outlay | $900.00 | $1,070.00 |

| Debt-free month | February 2029 | March 2028 |

| Total interest | $5,347.49 | $2,673.15 |

| Balance after 12 months | $18,287.92 | $11,529.80 |

| Store Card paid | April 2027 | July 2026 |

The point is not that every household can sustain a $1,300 outlay. The point is that a fast plan gets built in the payment stream, not in the label. If your friction is choosing where the extra money should go once it exists, the debt avalanche spreadsheet is a better tracking tool. If the problem is creating the extra money in the first place, keep reading.

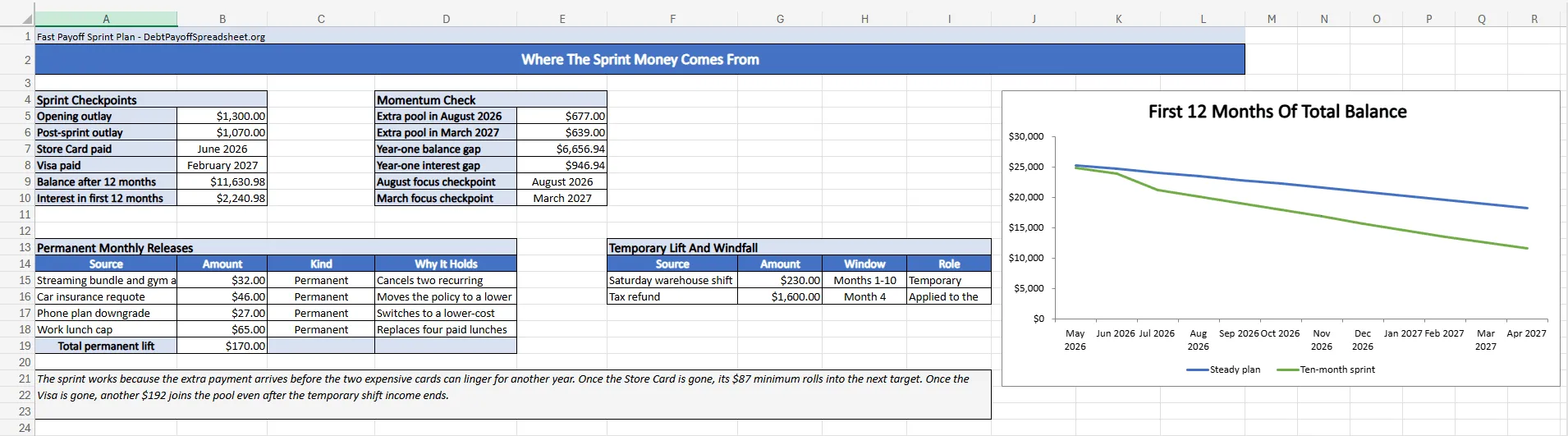

Front-Load The First Ten Months While The Expensive Balances Are Still Large

The sprint plan works because the bigger dollars arrive early, before the two expensive cards have time to sit there for another year. In this scenario, the permanent lift is $170 per month: $32 from a streaming bundle and unused gym add-on, $46 from requoting car insurance, $27 from a phone-plan downgrade, and $65 from capping paid work lunches. A temporary Saturday warehouse shift adds $230 for ten months. That gets the household from a $900 outlay to $1,300 through January 2027, then back to a still-strong $1,070 after the side income ends.

The first closure is where the plan starts compounding on itself. The Store Card reaches zero in July 2026. In August 2026, the focused pool is no longer just the scheduled extra. It is $677 because the old $87 minimum now rolls into the next target. The Visa then falls in February 2027. By March 2027, even after the temporary shift income has ended, the focused pool is $639 because another $192 minimum has joined the attack money.

That is why I would rather see someone run one short sprint than promise themselves a vague permanent sacrifice. A tight first year does more work than a tidy-looking five-year plan that never gets aggressive enough to wound the expensive card balances. If you need help finding those permanent trims inside a broader household plan, try the budget and debt payoff spreadsheet—it ties the debt plan back to actual spending categories.

Use Windfalls The Month They Land

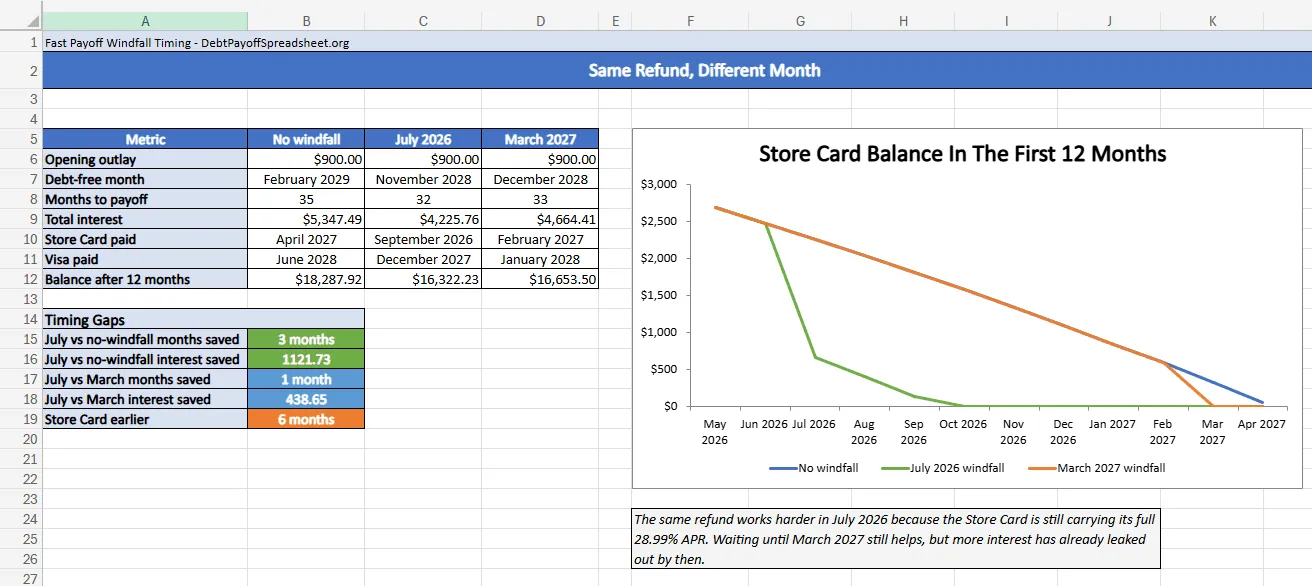

People often treat a tax refund or bonus as if timing is cosmetic. It is not. Keeping the monthly outlay fixed at $900 and changing only the month of a $1,600 refund produces three different outcomes here. No windfall reaches zero in February 2029 with $5,347.49 of interest. A July 2026 windfall reaches zero in November 2028 with $4,285.78 of interest. Holding the same refund until March 2027 reaches zero in December 2028 with $4,710.38 of interest.

The final gap is only one month between July and March, but the path feels different much earlier. The July refund clears the Store Card by September 2026. Waiting until March 2027 leaves that same card alive until March 2027. That delay costs $424.60 of extra interest and keeps the expensive balance in the plan for six additional months.

Early lump sums matter most when the target balance is both open and costly. If your smallest balance is a deferred-interest store purchase instead of a clean medical plan, check the fine print before copying this order. Deferred-interest offers can charge interest back to the purchase date if the balance is not fully cleared in time, and minimum payments usually will not get the job done (CFPB). For that edge case, the credit card debt payoff guide goes deeper.

Speed Has A Ceiling

There is one bad version of a fast plan that needs to be said plainly: sending every spare dollar to debt while the next routine setback is guaranteed to go back on a card. A plan can look brilliant on paper and still fail because one repair bill lands before the next paycheck. I would rather see a slightly slower plan with enough cash to absorb a normal disruption than a perfect sprint that immediately recreates revolving debt.

Minimum payments are the floor you do not cut through for speed. If the sprint outlay is threatening those minimums, the plan is already too aggressive. Act immediately and call the card issuer if you cannot make the minimum, instead of letting the account drift further behind (CFPB). The real order of operations: stay current, protect the plan from new borrowing, then sprint.

For this exact debt stack, the decision rule is clean. Keep the same order. Raise the payment stream early if you can. Use one-time money as soon as it arrives. Slow the sprint the moment it threatens the minimums or sends normal emergencies back onto a card. Fast payoff is usually built from timing and consistency, not from finding a smarter slogan.

How to Pay Off Debt Fast FAQ

How to pay off debt fast?

List every balance, APR, and minimum payment, keep one payoff order, then look for ways to push more money into the first year of the plan. In the scenario on this page, the finish line moves up by 11 months because the household adds a ten-month sprint and uses a July refund right away instead of changing methods every few weeks.

What should an Excel debt payoff template include?

A useful template should show balance, APR, minimum payment, start month, one repeatable extra-payment field, and a month-by-month payoff schedule. If you are trying to move faster, it also needs room to model temporary income, one-time windfalls, and the bigger payment pool that appears after a balance is paid off.

Is there a free debt payoff spreadsheet?

Yes. The main spreadsheet on our homepage is the better fit if you want one file for your own balances, APRs, minimum payments, and extra payment amount. The workbook downloads in this article are narrower on purpose because they isolate one fast-payoff scenario and let you inspect the sprint and windfall timing before you customize anything.

Can I use a debt payoff calculator Excel workbook?

Yes. A calculator is faster for the first answer on payoff month, interest total, and whether a sprint is worth testing at all. Excel makes more sense once you want an offline file you can audit, save, and revisit after each statement cycle, especially if your extra payment changes over time.

Related Guides and Resources

- Debt Payoff Calculator: Compare Snowball vs Avalanche Before You Commit

- Debt Payoff Spreadsheet Excel: Free Workbook With Dashboard and Strategy Tabs

- Debt Payoff Spreadsheet Google Sheets: Shared Tracker With Dashboard and Check-In Log

- Debt Payoff Spreadsheet Printable: Free Print-Ready Tracker With Monthly Check-In Sheets